The financial statements of an organization give a clear picture of their financial health. They also provide information needed to make decisions about the direction of the organization.

Income Statement

An income statement, also known as a revenue and expenditure statement, statement of operations, or profit and loss statement, for the fiscal period shows:

- what an organization received as income or, in other words, revenue

- what was spent over a period of time or, in other words, expenses

Revenue information comes from the cash receipts journal. The expenses come from the cash disbursements journal. The difference between what was received as revenue and what was spent is either a surplus or a deficit. A surplus means that more revenue was generated than expenditures. A deficit means there were more expenses than revenue. The surplus or deficit is reported on the bottom line.

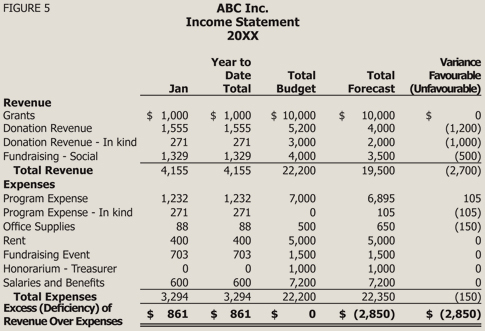

Income statements are prepared on a monthly or quarterly basis and compared to the budget and forecast on the statements. The forecast is the amount of income and expenses projected for the year. It is based on what has come in and been spent already and what you expect to receive and spend for the rest of the year. The picture below illustrates an example income statement. The variance column is the difference between the total year budget and forecast figures. Once the variances have been pinpointed, the reasons for them are explored and action is taken if required.

Balance Sheet

The balance sheet is a snapshot of assets and liabilities at a particular point in time. It is sometimes called a statement of financial position. For this statement, total assets will always be equal to the total of liabilities and equity. Assets are what the organization owns or what is owed to them. Liabilities are what an organization owes. Equity is what is left of the assets once all the liabilities have been paid. It is known as net assets in a non-profit.

Audits

Accountability is maintained when financial documents exist to justify every transaction that takes place. After preparation of financial statements, an accounting firm normally does an audit. The audit will include an opinion on whether the statements are accurate with regard to the financial position of the organization at year end.

The requirements for audit will vary depending on the structure of the organization and its revenue. For more information, see Non-profit Financial Statements.